Ai Content Generator

Ai Picture

Tell Your Story

9 Financial Topics You Need An Understanding Of

Navigating the world of personal finances can be confusing when you’re just getting started. Unfortunately, most people weren’t taught about finances in school. As a result, financial literacy across the country is far lower than it should be. First, remember that there’s no shame in being a beginner. It’s not your fault that you haven’t learned about these important financial topics before now.

However, it is your responsibility to take charge and learn about these topics and how they affect you. In this article, we’re breaking down nine important financial topics you need an understanding of.

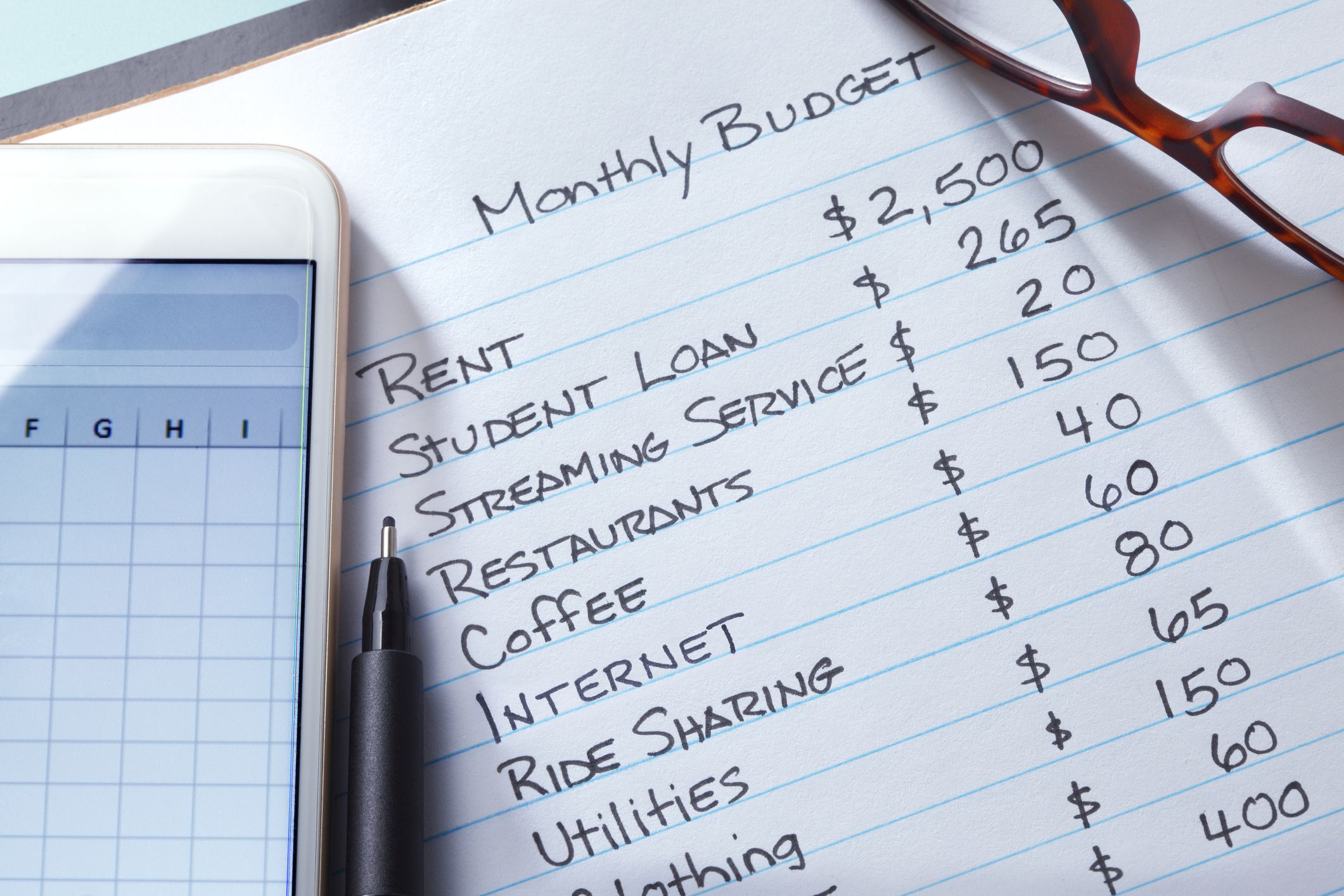

1. Budgeting

Budgeting is one of the most foundational financial topics of personal finance that everyone should know. In short, budgeting is deciding how you’ll allocate all of your money. It involves figuring out exactly how much you earn each month and where it’s going to go.

Keep in mind that budgeting is not about perfection. It's about the review, your progress, and implementation. If you struggle initially, over time, if you stay committed, you'll get better with budgeting.

Budgeting methods

There’s not necessarily one right way to budget. Instead, it’s about finding the strategy that works best for you. There are several different budgeting methods that people have had success with. A few popular ones include:

50/30/20 budget

Using this 50/30/20 percentage budgeting system, you allocate 50% of your budget to needs such as housing, insurance, and transportation. 30% of your income goes toward wants, which can be eating out, shopping, travel, and more. Finally, 20% of your income goes toward savings and debt. This budgeting system is popular, but likely not ideal for people with significant debt to pay off.

Zero-based budget

Using the zero-based budgeting method, you plan your spending by taking your total monthly income and allocating it to budget categories until you have $0. The premise of this system is that you find a job for every single dollar, even if that job is savings or debt payoff.

Pay yourself first

The pay-yourself-first budgeting method is also known as reverse budgeting. Using this method, you figure out how much you want to pay yourself each month, meaning how much you want to put toward your savings and debt goals. From there, you can spend whatever is left.

Envelope system

The envelope system can be used in conjunction with any other type of budget. Using this strategy, you have an envelope for each spending category. In each envelope is the cash available to spend for the current month. When the envelope is empty, you’re done spending in that category for the month.

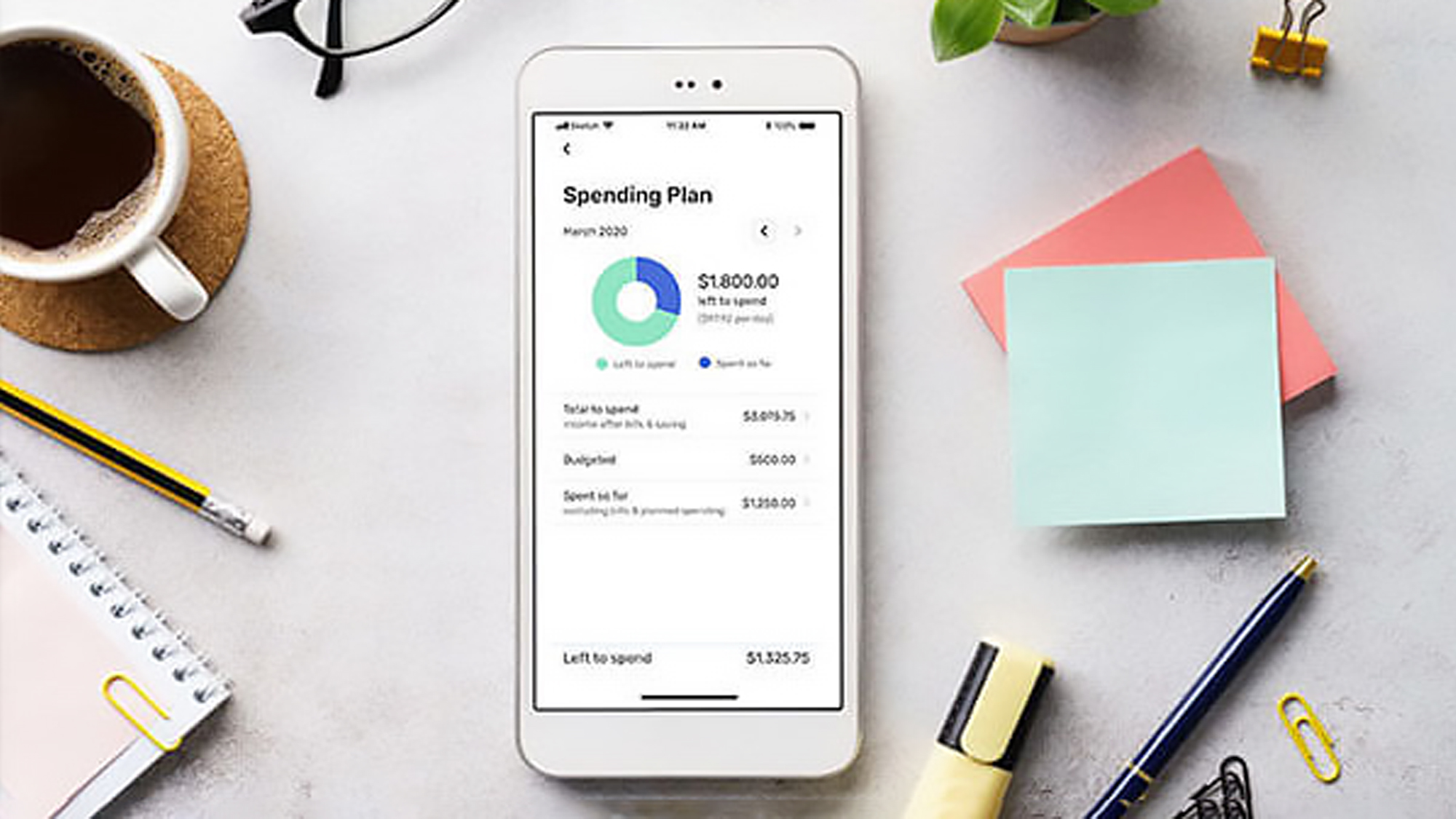

Budgeting apps

There are many budgeting apps on the market to help you plan your spending and track your expenses throughout the month. Some of the most popular budgeting apps on the market include:

- Mint

- You Need a Budget

- Personal Capital

- EveryDollar

2. Debt

Debt is more prevalent than ever in today’s society. The data shows that consumer debt has grown to more than $14.9 trillion in recent times, with the average consumer having about $92,727 in debt. And as it becomes more common, it becomes increasingly important to understand how to manage debt.

Revolving vs. non-revolving debt

Every debt is either revolving or non-revolving. Revolving debt is one where you can continuously spend and pay off the debt. The most common revolving debt is a credit card, though a line of credit is also a type of revolving debt.

Non-revolving debt is one where you borrow a lump sum and then pay it off over a specific term. Non-revolving debts include mortgages, student loans, personal loans, and car loans.

Secured vs. unsecured debt

A secured debt is one that is secured by collateral or an asset the lender can seize if you don’t make your payments. Mortgages and auto loans are secured debts since your lender can seize your home or car if you don’t pay them back.

Unsecured debts don’t have any collateral behind them. The lender can still take legal action to get their money, but there’s no asset they can seize from you. Student loans and credit cards are examples of unsecured debts.

Understanding your debt

It’s important to know about and fully understand each debt you have. For each debt, you should know your:

- Total balance

- Interest rate

- Minimum monthly payment

- Estimated payoff date

- Once you understand your debt, you can use a debt payoff method like the debt snowball or debt avalanche to pay it off.

3. Net worth

Your net worth is one of the most important aspects of your financial picture. Your net worth is simply the difference between what you own and what you owe.

To calculate your net worth, start by adding up all of your assets, which includes money in your bank and investment accounts and physical assets like your home. Next, add up all of your debts. Subtract your debts from your assets, and you get your net worth.

It’s okay if your net worth isn’t where you want it to be right now. Many younger people have a negative net worth as a result of student loans. The goal is simply to watch your net worth increase over time as you save money and pay off debt.

4. Credit

Credit refers to the ability to borrow money. But when people talk about credit, they’re usually talking about either their credit report or their credit score.

Credit report

Your credit report is a full list of all your current debt accounts, including how much you owe, who you owe it to, and the monthly payments you’ve made. It also includes possibly negative information, such as any accounts in collections, and whether you’ve filed for bankruptcy.

When lenders are deciding whether to give you money, they look to your credit report to see how responsibly you’ve handled debt in the past.

Credit score

Your credit score is a number between 300 and 850 which is essentially a numerical rating of your credit report. It’s a snapshot of how responsible you are with debt. Here are how the different scores fall on a scale of poor to excellent, according to Experian:

- Very poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very good: 740-799

- Exceptional: 800-850

The importance of credit

Your credit score is one of the most important numbers in your financial toolbox. Someone may run your credit anytime you apply for a loan or credit card, rent an apartment, or even apply for a job.

A poor credit score can result in you being denied loans or being stuck with high interest rates. A good score can literally make the difference of tens or hundreds of thousands of dollars over your lifetime. It can also result in you being turned down for apartments and jobs.

5. Saving

It probably doesn’t come as a surprise that saving is one of the most important components of personal finance, but most people simply aren’t doing it. In fact, data shows that just 39% of Americans could afford to pay for a $1,000 emergency without taking on more debt.

The first saving priority most people should have is an emergency fund. Your emergency fund can help you cover any unforeseen expenses. It can also serve as an income replacement in the event that you lose your job. Most experts recommend having between three and six month’s worth of expenses saved in your emergency fund.

The other type of saving you might do is for specific financial goals. Whether it’s a dream vacation or the downpayment on a home, saving will help you get there.

Unfortunately, there’s no magic pill or secret to saving money — you just have to do it. When it comes to saving for a big goal, the best way to reach it is to divide the total number you need to save by the number of months you’d like to have it saved. That will tell you how much to save each month to reach your goal.

6. Investing

Investing can be an intimidating topic when you first get started, but it’s actually one of the most important aspects of your finances. Why is that? Well, most people can’t save enough money to retire. Instead, when you invest, your money compounds and grows at a much faster rate. The hope is that it eventually compounds enough that you can retire.

A recent survey discovered that the average family believes they’ll need about $1.9 million to retire comfortably. Unfortunately, the average family also only has about $255,200 in retirement accounts. Luckily, by starting early and investing consistently, you can reach your retirement goals.

Remember that you can also invest in non-retirement taxable brokerage accounts, but it’s generally recommended that you first max out your tax-advantaged retirement accounts.

Investing 101

There are a few investing terms everyone should know before they start investing:

Asset allocation

How you divide your assets up across all of your investments

Time horizon

The number of years before you expect to need the money you’re investing

Diversification

The practice of spreading your money across many different investments

Risk tolerance

Your ability and willingness to lose money in the stock market

7. Homeownership

Homeownership is one of the most common goals and financial topics. After all, homeownership is just about the epitome of the American dream.

Unfortunately, a home is also incredibly expensive. According to Zillow, the average home in the United States is valued at about $276,717. And depending on where you live, the local average can easily exceed that by hundreds of thousands of dollars.

Here are a few things to keep in mind when it comes to buying a home:

Only buy what you can afford

A general rule of thumb is that your housing costs shouldn’t exceed about 30% of your monthly income. Unfortunately, lenders often approve borrowers for far more than that.

No one knows your financial situation like you do — not even a lender. Be sure that the monthly payment for your home fits comfortably within your budget. And remember, your monthly costs don’t just include your principal and interest.

Save for a down payment

For most types of loans, you must have a down payment to buy a home. Down payments typically range from 3.5% for an FHA loan to 20% for a conventional mortgage. You don’t necessarily need 20%, but you’ll pay PMI if you put down a smaller down payment.

There will also be other upfront costs in addition to the down payment. These include closing costs, a home inspection, and moving costs.

You also have to account for home insurance and taxes, which can be more expensive than people realize.

Maintain a home emergency fund

Maintaining a home is expensive, and experts generally recommend saving about 1% of your home’s value each year for maintenance and repairs. In addition to your personal emergency fund, it’s best to keep a separate emergency fund just for your home so you can easily afford any unexpected repairs.

8. Taxes

Taxes may be one of the most dreaded parts of managing money, but they’re also one of the most necessary financial topics to be aware of. Because whether you realize it or not, if you’re earning money, you’re also paying taxes. But for most people, they simply come out of your paycheck before you even see the money.

You don’t have to be a tax expert, but it is important to understand how much you pay in taxes each year, whether you’re required to file a federal and state tax return, and what deductions you might be eligible for. Luckily, a good accountant — or even a good tax software, can help you figure out those things.

9. Insurance

Insurance might be one of the least important financial topics to discuss. But if there’s ever an emergency — and chances are that there will be — you’ll be glad you have insurance.

In general, buying insurance involves paying another company a monthly premium to cover your liabilities in an emergency. Types of insurance that most people should have include:

- Health insurance

- Homeowners or renters insurance

- Auto insurance

- Life insurance

- Disability insurance

The bottom line

If you read through this list of financial topics and immediately felt overwhelmed, don’t worry. You don’t have to have a deep understanding of each of these topics today. But this list will be a great starting point for you as you learn.

You can reference it as you continue to research and learn about each topic. And ultimately, you’ll be glad to have each of these important topics in your financial toolbox.

Related Posts

© 2025 Invastor. All Rights Reserved

User Comments